Insured Mortgage Rules and Affordability in 2026: A Practical Guide for Canadian Homebuyers

January 25, 2026 | Posted by Guriqbal Chahal, Mortgage Broker

If you are trying to buy a home in Canada right now, you have probably felt the disconnect.

Interest rates are lower than they were at the peak, but affordability still feels tight. Home prices in many markets have not fallen enough to make buying feel easy. And qualifying can still feel like a math problem with moving pieces.

That is exactly why insured mortgage rules matter more in 2026 than most buyers realize.

What Are Insured Mortgage Rules in Canada?

Insured mortgage rules in Canada apply when a buyer puts less than 20% down on a home.

Mortgage default insurance is required, the insurance premium is typically added to the mortgage, and buyers must follow set price caps, amortization limits, and qualification rules.

An insured mortgage can be a powerful affordability tool. It can also surprise buyers who do not understand how insurance premiums and amortization choices affect monthly payments and total cash required at closing.

Why Insured Mortgage Rules Matter More in 2026

Even when interest rates stabilize or decline, affordability does not automatically reset. Buyers still need to qualify, manage monthly payments, and have enough cash to close.

- Allow buyers to purchase with smaller down payments

- Increase total mortgage size due to insurance premiums

- May allow longer amortizations for eligible buyers

- Can reduce monthly payment pressure while increasing total cost

Insured Mortgage Rules in 2026: Quick Facts

- Down payment: Less than 20%

- Maximum insured purchase price: Up to $1.5 million

- Amortization: Up to 30 years for eligible first-time buyers or new builds

- Insurance premium: Usually added to the mortgage balance

The Insured Mortgage Affordability Equation

For most homebuyers, affordability comes down to four factors:

- Purchase price

- Down payment

- Interest rate

- Amortization length

Insured mortgage rules directly affect your down payment flexibility, total mortgage amount, and sometimes your amortization options.

Why Amortization Length Matters

A longer amortization spreads repayment over more years, lowering the monthly payment. In tighter markets, this can be the difference between qualifying comfortably and not qualifying at all.

The trade-off is higher total interest paid over time and potential insurance premium surcharges when amortization exceeds 25 years.

Mortgage Insurance Premiums: Paying for Flexibility

Mortgage default insurance allows buyers to enter the market sooner with smaller down payments. That flexibility comes at a cost, as the premium increases the total mortgage size and monthly payment.

This is why side-by-side comparisons matter when choosing an insured mortgage structure.

A Practical Insured Mortgage Playbook for 2026 Buyers

Step 1: Confirm Whether You Are in Insured Territory

Less than 20% down usually means an insured mortgage. Twenty percent or more typically means uninsured financing.

Step 2: Use the Insured Price Cap Correctly

The $1.5 million insured cap helps buyers in higher-priced markets but remains a hard limit.

Step 3: Ask About 30-Year Insured Amortization Eligibility

Eligibility often depends on whether you are a first-time buyer or purchasing a new build.

Step 4: Budget for Total Cash to Close

Closing costs include legal fees, adjustments, land transfer taxes (where applicable), and moving expenses — not just the down payment.

Step 5: Decide What You Are Optimizing For

- Lowest monthly payment

- Lowest total mortgage cost

- Lowest upfront cash requirement

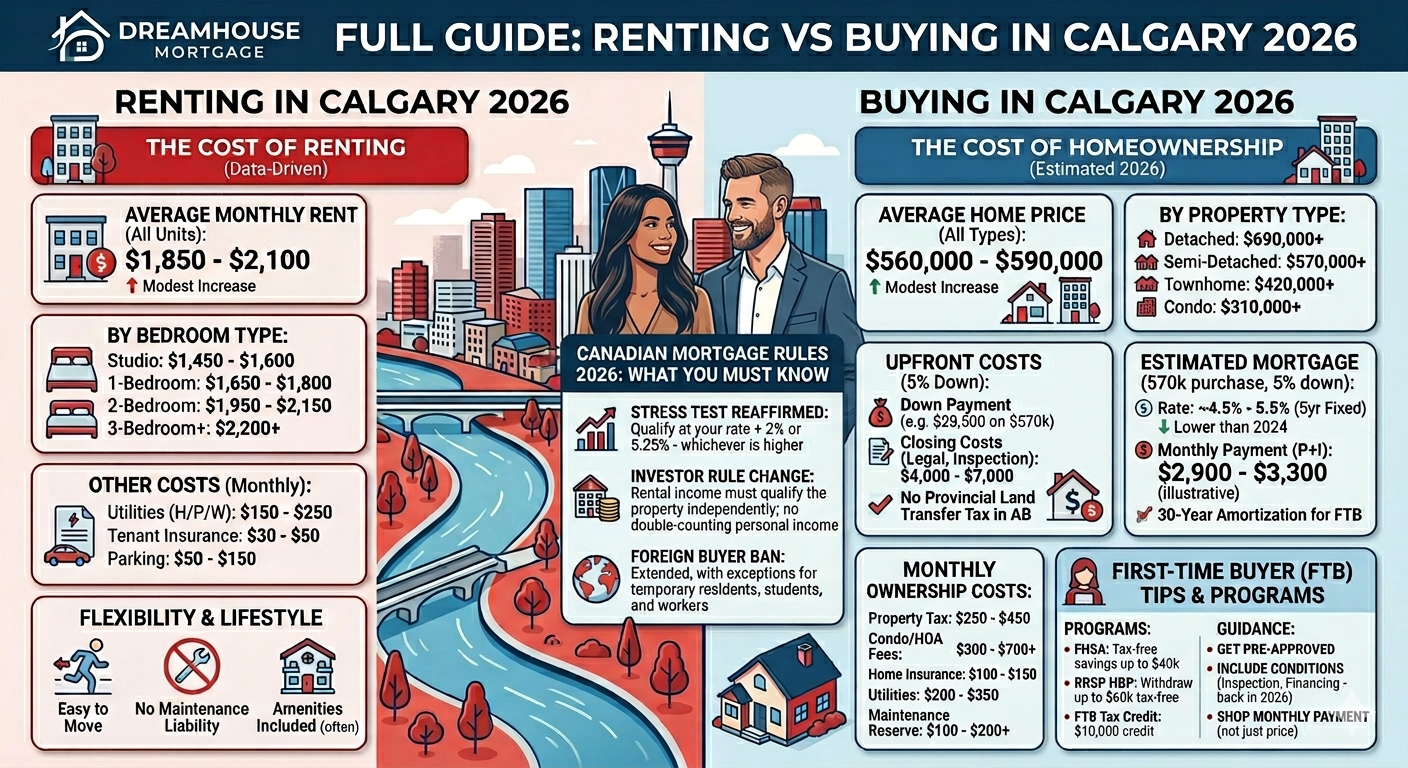

How Insured Mortgage Rules Affect Buyers in Calgary and Alberta

In Calgary and across Alberta, insured mortgage rules remain highly relevant. Rising demand, population growth, and limited inventory mean many buyers rely on insured financing to enter the market.

For Calgary first-time homebuyers, insured mortgages can significantly reduce the time needed to save a 20% down payment while keeping monthly payments manageable.

Because lender policies and qualifying rules vary, Alberta buyers benefit from working with mortgage professionals who understand both federal insured rules and provincial nuances.

Bottom Line: Use Insured Mortgage Rules Intentionally

In 2026, insured mortgages are one of the most practical affordability tools available to Canadian buyers — especially first-time buyers and those with smaller down payments.

The real benefit appears when buyers understand limits, premiums, amortization trade-offs, and cash-to-close requirements before house hunting.

Frequently Asked Questions

What is an insured mortgage in Canada?

An insured mortgage is typically required when you buy a home with less than 20% down. Mortgage default insurance protects the lender and the premium is usually added to the mortgage.

Do insured mortgages affect monthly payments?

Yes. The insurance premium increases the mortgage amount, but insured options can allow buyers to enter the market sooner.

Can I get a 30-year amortization with an insured mortgage in 2026?

In some cases, yes. Eligibility depends on buyer status, property type, and lender programs.

Should I always aim for 20% down?

Not always. Whether waiting makes sense depends on timing, affordability, and overall financial comfort.

Disclaimer: This article is for general informational purposes only and is not mortgage, financial, or legal advice. Always speak with a licensed Canadian mortgage professional before making decisions.

Guriqbal Chahal and the Dreamhouse Mortgage Team

📞 Call: (403) 966-6072

🏦 Dream House Mortgage

📅 Book Your Mortgage Consultation Appointment

👉 Take the next step today and get a mortgage strategy that works for 2026 and beyond.

Check these related services links: